This topic covers USA tax functions. To learn about Canadian tax functions, click here.

Click "USA" or a state name to see tax function details and documentation for the selected tax entity.

|

...\Extras\Payroll\Tax\Test State Tax functions.xls contains models for each of the tax functions. |

Alaska

No state income tax!

Alabama

- Filing status: Comes from lines 1-3 of Form A-4 and must be one of the following:

- 0 - No personal exemption

- S - Single exemption

- MS - Married filing separately exemption

- M - Married exemption

- H - Head of family exemption

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: 2025 (use bookmarks in PDF to skip to relevant sections)

- Link to A4: 2025

- If an employee's A4 is missing, state tax is calculated using a filing status of "0".

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('AL')

Alternate method:

Arkansas

- Supplemental pay: Taxed separately at a flat rate.

- Link to instructions: Arkansas

- Link to tax withholding formula: Formula

- Link to AR4EC: 2025

- If an employee's AR4EC is missing, state tax is calculated using a filing status of "Single" with 0 exemptions.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('AR')

Alternate method:

Arizona

- Arizona applies a flat tax rate. If you choose not to use the built-in StateW4.Withholding tax function, store the rate in a segment item parameter.

- Link to instructions: current

- Link to A-4: 2025

- If an employee's A-4 is missing, state tax is calculated using a flat rate of 2.0%.

Example

Preferred method using data from employee state W-4 records:

StateW4.Withholding('AZ')

California

- Filing status: "S", "M", or "H"

- Supplemental and bonus pay: Taxed at flat percents only when paid on a separate check (i.e., source amount = supplemental + bonus).

- Link to instructions: 2025 Employer's Guide (use bookmarks in PDF to skip to relevant sections)

- Link to current tax tables: 2025

- Link to DE 4: 2025

- If an employee's DE 4 is missing, state tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('CA')

Alternate method:

Colorado

- Filing status: "M" or "S"

- Supplemental pay: Taxed at a flat percent only when paid on a separate check (i.e., source amount = supplemental amount).

- Link to tax tables and instructions: 2024 witholding guide, 2025 withholding worksheet

- Link to USA W-4: current

- Link to DR 0004: 2025

- If an employee's DR 0004 is missing, state tax is calculated based on the employee's IRS Form W-4. If the Form W-4 is missing, state tax is calculated using a filing status of "Single" and a Two Jobs value of "False".

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('CO')

Alternate method:

Connecticut

- Filing status: "A", "B", "C", "D", "E", or "F"

- Supplemental pay: No special treatment of supplemental pay. "The employer must compute the tax on the combined regular and supplemental wages."

- Link to employer's tax guide: 2025

- Link to withholding calculation rules: 2025

- Link to CT-W4: 2025

- If an employee's CT-W4 is missing, state tax is calculated using a flat rate of 6.99% with no exemptions.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('CT')

Alternate method:

CT(Source, Tax:CT:Filing Status)

District of Columbia

- Filing status:

- S - Single

- M1 - Married Filing Jointly

- M2 - Married Filing Separate Returns or a Combined Separate Return

- H - Head of Household

- Supplemental pay: No special treatment.

- Link to tax tables and instructions: 2022 (use bookmarks in PDF to skip to relevant sections)

- Link to D-4: 2018

- If an employee's D-4 is missing, state tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

DC(Source, Tax:DC:FilingStatus, Tax:DC:Exemptions)

Delaware

- Filing status:

- S - Single

- M - Married Filing Joint Return

- M1 - Married Filing Separate Return

- Supplemental pay: Special taxation only occurs when paid on a separate check (i.e., source amount = supplemental amount). Tax on supplemental pay = tax on annual salary with supplemental pay minus tax on salary without supplemental pay.

- Link to tax tables and instructions: Delaware - supplemental wages, withholding

- Link to DE W-4: 2023

- If an employee's DE W-4 is missing and a pre-2020 federal Form W-4 is in effect for the employee as of the check date, state tax is calculated based on the federal Form W-4. If no pre-2020 Form W-4 is available, tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('DE')

Alternate method:

Florida

No state income tax!

Georgia

- Filing status:

- S - Single

- M2 - Married Filing Joint Return, both spouses working

- M1 - Married Filing Joint Return, one spouse working

- M - Married Filing Separate Return

- H - Head of Household

- Supplemental pay: Taxed separately at a graduated flat percent.

- Link to tax tables and instructions: 2025 (use bookmarks in PDF to skip to relevant sections)

- Link to G-4: 2025

- If an employee's G-4 is missing, state tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('GA')

Alternate method:

Hawaii

- Filing status:

- S - Single

- M - Married

- H - Head of Household

- Supplemental pay: Special taxation only occurs when paid on a separate check (i.e., source amount = supplemental amount). Tax on supplemental pay = tax on annual salary with supplemental pay minus tax on annual salary without supplemental pay.

- Link to instructions: 2025

- Link to HW-4: 2022

- If an employee's HW-4 is missing, state tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('HI')

Alternate method:

Iowa

- Supplemental pay: Taxed separately at a flat percent.

- Link to withholding formula: 2025

- Link to IA W-4: 2025

- If an employee's IA W-4 is missing or is dated before 1/1/2024, state tax is calculated using a filing status of "Other" with a total allowance amount of $40 and no additional withholding.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('IA')

Alternate method:

Idaho

- Filing status: "S" or "M"

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: Idaho State Tax Commission

- Link to percentage computation method: 04-28-2025 revision

- Link to ID W-4: 2025

- If an employee's ID W-4 is missing and a pre-2020 federal Form W-4 is in effect for the employee as of the check date, state tax is calculated based on the federal Form W-4. If no pre-2020 Form W-4 is available, tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('ID')

Alternate method:

Illinois

- Allowances: Line 1 and Line 2 allowances come from the employee's IL-W-4.

- Supplemental pay: No special treatment.

- Link to tax tables and instructions: 2025 (use bookmark in PDF to skip to relevant section)

- Link to IL-W-4: 2024

- If an employee's IL W-4 is missing, state tax is calculated using 0 basic personal allowances and 0 additional allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('IL')

Alternate method:

IL(Source, Tax:IL:Line1Allowances, Tax:IL:Line2Allowances)

Indiana

- Exemptions: The number of exemptions and dependents come from Lines 4 and 5 of the employee's Form WH-4.

- Supplemental pay: No special treatment.

- Link to tax tables and instructions: 10/2024 1/2025

- Link to WH-4: 2023

- If an employee's WH-4 is missing, state tax is calculated using 0 exemptions and 0 dependents.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('IN')

Alternate method:

IN(Source, Tax:IN:Exemptions, Tax:IN:Dependents)

Indiana counties

- Filing status:

- R - Resident

- N - Non-Resident

- Exemptions and dependents: From Indiana Form WH-4.

- County Code: A text argument with values from "01" through "92".

- Supplemental pay: No special treatment.

- Link to tax tables and instructions: 2025

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.LocalWithholding('IN')

Alternate method:

INC(Source, Tax:INC:FilingStatus, Tax:IN:Exemptions, Tax:IN:Dependents, "01"))

Kansas

- Filing status: "S" or "M"

- Supplemental pay: Taxed at a flat percent only when paid on a separate check (i.e., source amount = supplemental amount).

- Link to tax tables and instructions: 2024; 2024 instructions

- Link to K-4: 2024

- If an employee's K-4 is missing, state tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('KS')

Alternate method:

Kentucky

- Supplemental pay: No special treatment.

- Link to instructions and formula: 2025 instructions; 2025 formula

- Link to K-4: 2025

- If an employee's K-4 is missing, state tax is calculated with no exempt claim allowed and no additional withholding.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('KY')

Alternate method:

KY(Source, Tax:KY:Exemptions)

Louisiana

- Filing status: "S", "M", or "N"

- Exemptions: 0, 1, 2 (from the L-4).

- Dependents: From the L-4.

- Supplemental pay: No special treatment.

- Link to tax tables and instructions: 2025, withholding formula 2022

- Link to L-4: 2025

- If an employee's L-4 is missing, state tax is calculated using a filing status of "No exemptions or dependents claimed", 0 dependents, and 0 exemptions.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('LA')

Alternate method:

LA(Source, Tax:LA:FilingStatus, Tax:LA:Exemptions, Tax:LA:Dependents)

Massachusetts

- Filing status: Corresponds to the boxes marked on the employee's Form M-4. For example:

- Blank. No boxes marked.

- A. Box A (Head of Household) is marked.

- AC. Boxes A (Head of Household) and C (spouse is blind) are marked.

- Exemptions: The total from Box 4 of Form M-4.

- FICA withheld: The total deducted from this check for Social Security (FICA), Medicare, Massachusetts, or Railroad Retirement systems.

- FICA year-to-date: The year-to-date total deducted (before the current check).

- Supplemental pay: No special treatment.

- Link to tax tables and instructions: 2025 (use bookmark in PDF to skip to relevant section)

- Link to M-4: 2020

- If an employee's M-4 is missing, state tax is calculated using 0 exemptions.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('MA')

Alternate method:

MA(Source, Tax:MA:FilingStatus, Tax:MA:Exemptions, SumCheck('FICA Result'), SumYTD('FICA Result'))

Maryland

- Filing status: "S" or "M"

- County codes:

- AL - Allegany

- AA - Anne Arundel

- BC - Baltimore City

- BA - Baltimore County

- CV - Calvert

- CA - Caroline

- CR - Carroll

- CE - Cecil

- CH - Charles

- DO - Dorchester

- FR - Frederick

- GA - Garrett

- HA - Harford

- HO - Howard

- KE - Kent

- MO - Montgomery

- PG - Prince George's

- QA - Queen Anne's

- SM - St. Mary's

- SO - Somerset

- TA - Talbot

- WA - Washington

- WI - Wicomico

- WO - Worcester

- NR - Nonresident

- DE - Delaware

- Supplemental pay: Taxed separately at a flat percent.

- Links: 2025 Withholding Guide, 2025 Withholding Facts

- Link to MW507: 2025

- If an employee's MW507 is missing, state tax is calculated using a filing status of "Single" with 1 exemption; employee is not exempt from state or local.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('MD')

Alternate method:

MD(Source, Tax:MD:FilingStatus, Tax:MD:Exemptions, Max(0, SumCheck('Supplemental Result') - (SumCheck('PreIncomeTax Result') * SumCheck('Supplemental Result') / SumCheck('Compensation Result'))), AttributeItem('MDCounty', CheckDate))

Maine

- Filing status: "S" or "M"

- Supplemental pay: Taxed at a flat percent only when paid on a separate check (i.e., source amount = supplemental amount).

- Link to withholding tables and instructions: 2025

- Link to W-4ME: 2025

- If an employee's W-4ME is missing, state tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('ME')

Alternate method:

Michigan

- Supplemental pay: Taxed at a flat percent only when paid on a separate check (i.e., source amount = supplemental amount).

- Link to tax tables and instructions: 2025 guide

- Link to MI-W4: 2021

- If an employee's MI-W4 is missing, state tax is calculated using 0 exemptions.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('MI')

Alternate method:

Michigan Cities

- Filing status:

- R - Resident

- N - Non-Resident

- Exemptions: Depending on the city, the number comes from the federal, state, or local W-4. For example, Detroit requires a Form DW-4.

- City code: See list in the link below.

- Supplemental pay: No special treatment.

- Link to tax tables and instructions: Michigan City

Example of tax function

MIC(Source, Tax:MIC:FilingStatus, Tax:MIC:Exemptions, "ALB")

Minnesota

- Filing status: "M" or "S"

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: 2025 instructions

- Link to W-4MN: 2025

- If an employee's W-4MN is missing, state tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('MN')

Alternate method:

Missouri

- Filing status:

- S - Single

- M - Married, Spouse Works

- M1 - Married, Spouse Does Not Work

- H - Head of Household

- Supplemental pay: Taxed at a flat percent only when paid on a separate check (i.e., source amount = supplemental amount).

- Link to tax tables and instructions: 2025 tax guide (use bookmarks in PDF to skip to relevant sections), calculator

- Link to MO W-4: 2025

- If an employee's MO W-4 is missing, state tax is calculated using a filing status of "Single".

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('MO')

Alternate method:

Mississippi

- Filing status:

- S - Single

- M - Married, One Spouse Employed

- B - Married, Both Spouses Employed

- H - Head of Family

- Exemption: Amount is the total from Line 6 of MS Form 89-350 (Mississippi Employee's Withholding Exemption Certificate)

- Supplemental pay: No special treatment.

- Link to tax tables and instructions: 2025 (use bookmarks in PDF to skip to relevant sections)

- Link to 89-350: 2025

- If an employee's 89-350 is missing, state tax is calculated using a filing status of "Single" with 0 exemptions.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('MS')

Alternate method:

MS(Source, Tax:MS:FilingStatus, Tax:MS:ExemptionAmount)

Montana

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: Montana - 2025 guide

- Link to MW-4: 2025

- If an employee's MW-4 is missing and a pre-2020 federal Form W-4 is in effect for the employee as of the check date, state tax is calculated based on the federal Form W-4. If no pre-2020 Form W-4 is available, tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('MT')

Alternate method:

North Carolina

- Filing status: "M", "S", or "H".

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: 2025

- Link to NC-4: 2025

- If an employee's NC-4 is missing, state tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('NC')

Alternate method:

North Dakota

- Filing status: "S" or "M"

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: 2025 (use bookmarks in PDF to skip to relevant sections)

- Link to USA W-4: current

- The state tax calculation differs depending on whether the employee's current federal Form W-4 is dated before 2020 or is dated 2020 and thereafter. If the employee does not have a federal Form W-4 on file, state tax is calculated using a filing status of "Single" and Two Jobs = "False".

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('ND')

Alternate method:

Nebraska

- Filing status: "S" or "M"

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: 2025 [use bookmarks in PDF to skip to relevant sections]

- Link to W-4N: 2022

- If an employee has a pre-2020 federal Form W-4 in effect as of the check date, state tax is calculated based on the pre-2020 federal Form W-4. If an employee's W-4N is missing and the Form W-4 in effect is dated 2020 or later, tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('NE')

Alternate method:

New Jersey

- Filing status:

- A. Box 1 or Box 3 on Line 2 of Form NJ-W4 is marked, employee selected Rate A on Line 3, or "Single" or "Married But Withhold at a Higher Single Rate" is marked on the federal W-4.

- B. Box 2, 4, or 5 on Line 2 of Form NJ-W4 is marked, employee selected Rate B on Line 3, or "Married" is marked on the federal W-4.

- C, D, or E. Employee selected this rate on Line 3 of Form NJ-W4.

- Supplemental pay: No special treatment.

- Link to instructions: 2024

- Link to tax tables: 2021

- Link to NJ-W4: 2021

- If an employee's NJ-W4 is missing, state tax is calculated using a wage letter of "A" and 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('NJ')

Alternate method:

NJ(Source, Tax:NJ:FilingStatus, Tax:NJ:Exemptions)

New Hampshire

No state income tax!

New Mexico

- Filing status: "S" or "M"

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: 2025 (use bookmarks in PDF to skip to relevant sections)

- Link to USA W-4: current

- The employee's filing status from the federal Form W-4 in effect for the employee as of the check date is used to calculate state tax. If the employee's federal Form W-4 is missing, state tax is calculated using a filing status of "Single".

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('NM')

Alternate method:

Nevada

No state income tax!

New York

- Filing status: "S" or "M"

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: 2023 (use bookmarks in PDF to skip to relevant sections)

- Link to IT-2104: 2025

- If an employee's IT-2104 is missing and a pre-2020 federal Form W-4 is in effect for the employee as of the check date, state tax is calculated based on the federal Form W-4. If no pre-2020 Form W-4 is available, tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('NY')

Alternate method:

New York cities

New York City

- Filing status: "S" or "M"

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: 2018 (use bookmarks in PDF to skip to relevant sections)

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.LocalWithholding('NY')

Alternate method:

Yonkers

- Filing status: "S" or "M"

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: 2023 (use bookmarks in PDF to skip to relevant sections)

Ohio

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: 2025 instructions, 10/2025 computer formula

- Link to IT-4: 2024

- If an employee's IT-4 is missing, state tax is calculated using 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('OH')

Alternate method:

Oklahoma

- Filing status: "S" or "M"

- Supplemental pay: Taxed separately at a flat percent.

- Link to tax tables and instructions: Oklahoma - 2025 (use bookmarks in PDF to skip to relevant sections)

- Link to OK-W-4: 2021

- If an employee's OK-W-4 is missing, state tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('OK')

Alternate method:

Oregon

- Filing status: "S" or "M"

- Supplemental pay: Taxed at a flat percent only when paid on a separate check (i.e., source amount = supplemental amount).

- Link to tax tables and instructions: 2025 formulas

- Link to OR-W-4: 2025

- If an employee has a pre-2020 federal "Oregon only" Form W-4 in effect as of the check date and no OR-W-4 on file, state tax is calculated based on the filing status from the pre-2020 federal "Oregon only" Form W-4. If an employee's OR-W-4 is missing and the Form W-4 in effect is dated 2020 or later, tax is calculated using a flat rate of 8%.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('OR')

Alternate method:

Pennsylvania

- Pennsylvania applies a flat tax rate. If you choose not to use the built-in StateW4.Withholding tax function, store the state AND local tax rates in segment item parameters.

- Link to instructions: 1/2023 revision

- Link to REV-419 (nonwithholding): 2021

Example

Preferred method using data from employee state W-4 records:

StateW4.Withholding('PA')

Rhode Island

- Supplemental pay: Taxed at a flat percent only when paid on a separate check (i.e., source amount = supplemental amount). Tax on supplemental pay = tax on annual salary with supplemental pay minus tax on annual salary without supplemental pay.

- Link to tax tables and instructions: 2025 (use bookmarks in PDF to skip to relevant sections)

- Link to RI W-4: 2025

- If an employee's RI W-4 is missing, state tax is calculated using 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('RI')

Alternate method:

South Carolina

- Supplemental pay: No special treatment.

- Link to tax tables and instructions: formula

- Link to SC W-4: 2025

- If an employee's SC W-4 is missing and a pre-2020 federal Form W-4 is in effect for the employee as of the check date, state tax is calculated based on the filing status and allowances from the federal Form W-4. If no pre-2020 Form W-4 is available and the SC W-4 is missing, tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('SC')

Alternate method:

SC(Source, Tax:SC:Exemptions)

South Dakota

No state income tax!

Tennessee

No state income tax!

Texas

No state income tax!

![]()

USA

2020 introduced a new W-4 form. The withholding calculation for an employee differs depending on the year of their current W-4.

For W-4s prior to 2020, these facts apply:

- Withholding allowance: $4,300.00 per allowance

- Filing status: "S" or "M"

- Supplemental pay: Taxed separately at a flat percent.

For W-4s on or after 2020, these facts apply:

- No withholding allowance.

- Filing status: "S", "M", or "H"

- Supplemental pay: Taxed separately at a flat percent.

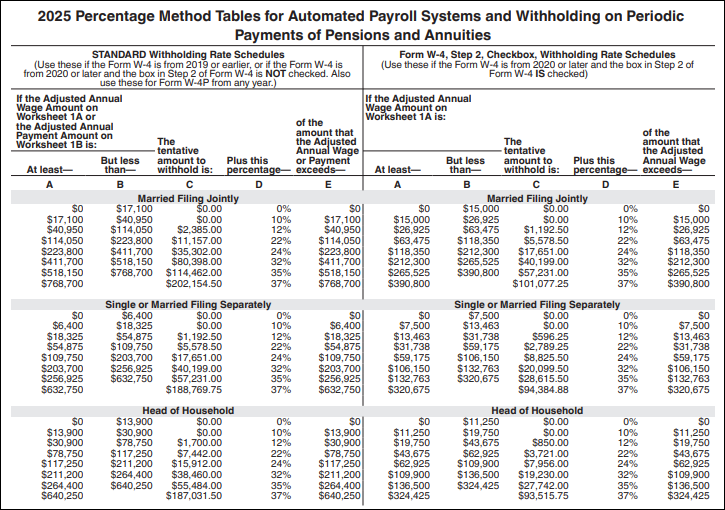

Percentage method withholding table for annual payroll period (2020 and pre-2020):

Link to Publication 15-T: 2025

Link to withholding calculator: USA

Link to W-4: current

Examples of tax functions

Preferred method using data from employee W-4 records:

W4.Withholding(FixedRate)

Alternate method:

Utah

- Filing status: "S" or "M"

- Supplemental pay: No special treatment.

- Link to tax tables and instructions: website; 2025 (use bookmark in PDF to skip to relevant section)

- Link to USA W-4: current

- If an employee's USA W-4 is missing, state tax is calculated using a filing status of "Single".

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('UT')

Alternate method:

UT(Source, Tax:UT:FilingStatus, Tax:UT:Allowances)

Virginia

- Filing status: "M" or "S"

- Supplemental and pension/annuity pay: Taxed at flat percents only when paid on a separate check (i.e., source amount = supplemental + pension/annuity).

- Link to tax tables and instructions: 2025 revision (use bookmarks in PDF to skip to relevant sections)

- Link to withholding calculator: Virginia

- Link to VA-4: 2011

- If an employee's VA-4 is missing, state tax is calculated using 0 personal allowances and 0 age and blindness allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('VA')

Alternate method:

Vermont

- Filing status: "S" or "M"

- Supplemental pay: Taxed at a flat percent only when paid on a separate check (i.e., source amount = supplemental amount).

- Link to tax tables and instructions: 2025 (use bookmarks in PDF to skip to relevant sections)

- Link to W-4VT: 2019

- If an employee's W-4VT is missing, state tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('VT')

Alternate method:

Washington

No state income tax!

Wisconsin

- Filing status: "S" or "M"

- Supplemental pay: Taxed separately at a graduated flat percent.

- Link to tax tables and instructions: 2024 (still valid for 2026) (use bookmarks in PDF to skip to relevant sections)

- Link to WT-4: 2024

- If an employee's WT-4 is missing and a pre-2020 federal Form W-4 is in effect for the employee as of the check date, state tax is calculated based on the filing status and allowances from the federal Form W-4. If no pre-2020 Form W-4 is available and the WT-4 is missing, tax is calculated using a filing status of "Single" with 0 allowances.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('WI')

Alternate method:

West Virginia

- Filing status:

- 1. One earner/one job. Single, head of household, or married with non-employed spouse.

- 2. Two earners/two or more jobs. Married filing jointly, both working; individual earning wages from two jobs.

- Supplemental pay: No special treatment.

- Link to tax tables and instructions: 2025

- Link to WV/IT-104: 2023

- If an employee's WV/IT-104 is missing, state tax is calculated using a filing status of "2" and 0 exemptions.

Example of tax function

Preferred method using data from employee state W-4 records:

StateW4.Withholding('WV')

Alternate method:

WV(Source, Tax:WV:FilingStatus, Tax:WV:Exemptions)

Wyoming

No state income tax!